5 minutes

Luxury post-Covid-19: Will China keep its promises?

China, which was placed in quarantine at the end of January due to the coronavirus pandemic, has begun to gradually resume activities after a month and a half under lockdown. The luxury industry has begun to reopen a large portion of its stores in the country and hopes to see clear signs of recovery. Initial activity signals a mixed response while hinting at the outlines of a market which will be significantly different to how it was pre-Covid-19.

As the main luxury groups announce their quarterly financial results, China has shown some positive results. On April 16, giants L’Oréal and LVMH reported a positive trend. Between January and March 2020, the global leader in cosmetics reported a 6.4% increase in sales in China which, “already shows an encouraging recovery of the consumption of beauty products,” according to L’Oréal’s CEO, Jean-Paul Agon. Moreover, LVMH’s chief financial officer Jean-Jacques Guiony indicated that, for the main brands of the group, namely Louis Vuitton, Dior, and Sephora, April’s, “recovery was rapid, with growth rates of 50% as of April 15.”

Hermès saw record sales at its store in Guangzhou in the province of Canton, which reopened in early April after an expansion project. The store recorded sales of €2.46 million on its first day of operations. This did not fail to raise hopes of recovery. However, these figures, which were published by US magazine WWD, were not confirmed by the brand, which did not respond to our communications. This could allude to a more uncertain situation.

Commenting on Hermès quarterly results on April 23, Hermès’ CEO Axel Dumas confirmed, “a positive trend in mainland China with double digit growth,” since the gradual reopening in March of its 11 stores there which had been closed since the end of January. However, the brand’s stores in Hong Kong and Macao, “have seen reduced traffic due to border control measures,” the brand said in a statement. “Several countries in this zone are experiencing a second wave of store closures since early April under government regulations, particularly in Singapore, Australia, and Thailand.”

Improvements in business activity

A few days earlier on April 21, Kering’s chief financial officer Jean-Marc Duplaix spoke about a complicated business backdrop. “It is difficult to have an overview as the situation is constantly varied from one city to another,” said Duplaix. “Restrictive measures are still being enforced in cities such as Beijing which is of course an important city for our business. Overall, we have seen a rise in sales in numerous cities, especially in the southern and eastern parts of the country, and this is also starting to materialise in the northern and western parts of the country, despite more contrasting trends.”

“Our stores could register double digit sales growth compared to last year in some cities,” said Duplaix. The business has also recorded an increase in online sales with a triple digit increase in online sales in China in February. China is the business’ second largest online market following the US.

The picture of a halftone recovery in China has also been seen in consulting firm Promise Consulting’s recent study ‘#Covid-19 : Tracking the Rebound’, which was produced with marketing research institute Panel On The Web and research firm AllianceBernstein. The study surveyed 600 Chinese citizens between March 26 and 29 and then again from April 6 to 10 to establish a recovery index of activities in China. “Although the Chinese appear eager to gradually resume economic, cultural, and social activity, numerous obstacles remain and the potential of an economic downturn remains a possibility,” said the authors of the study.

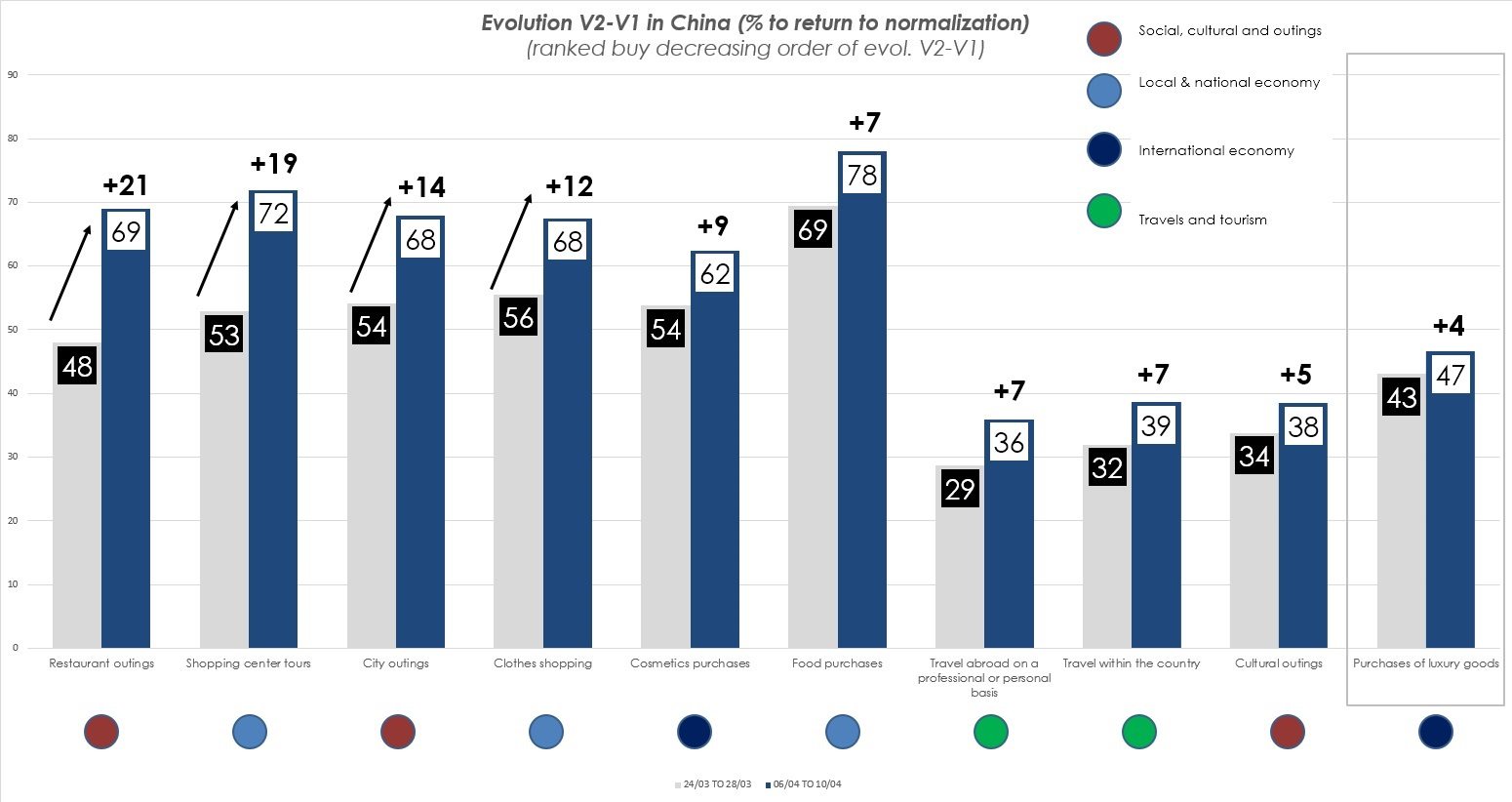

“There have been rather positive developments regarding primary and secondary activities, such as people going to restaurants, in commercial centres, and buying clothes,” said Promise Consulting’s CEO Philippe Jourdan. “An increasing number of our Chinese respondents believe that the situation will normalise in terms of local travel. On the other hand, they do not see a return to normal in terms of movement inside and outside of the country. In this context, purchases of luxury goods are activities which could be destined to be the last to restart.”

“The luxury sector is showing signs of a more moderate and below-average recovery as it ranks seventh among the sectors which have undergone the most pronounced slowdown (although it is true that a large number of sectors have slowed down in similar proportions). The luxury sector only makes the seventh rank of the sectors that the Chinese expect to return to normal, as far as they are concerned,” read the study.

The drop in economic growth in China (the country’s gross domestic product fell by 6.8% year-on-year during the January to March period) will certainly be accompanied by a drop in consumption including amongst the most wealthy Chinese who, “in-turn could cut their spending on luxury goods, faced with the prospect of slower growth,” said Jourdan.

Local consumption in mainland China

It should also be remembered that the majority of luxury goods purchases by the Chinese are made during tourist trips outside of the country. “There is real uncertainty concerning the resumption of travel outside of the country and current travel restrictions are expected to last so this will inevitably have an effect on the sales of luxury goods,” said Jourdan. “Moreover, as is always the case in China, it is the public authorities who decide on consumer priorities. Luxury goods purchases are seen as outflows of currency [outside the country]. Importance given to making purchases in China and buying from Chinese brands will increase.”

This trend has been highlighted by the Promise Consulting barometer. “Without anticipating the decisions of the Chinese authorities in the coming months, it is a likely scenario that there will be a desire, which was already strong before the pandemic, to reduce China’s economic dependence on the outside world,” read the study. “The Chinese will have a heightened desire to reclaim their consumption space.”

This scenario was confirmed by Duplaix on conference calls with analysts on April 21. “The conviction that we have at Kering is that certain trends, which have already appeared in recent quarters, will be confirmed and amplified to a certain extent,” said Duplaix. “The trend towards the repatriation of purchases to the domestic market in China is evident. For example, Shenzhen is a city that benefits significantly from this repatriation and I think that we will also see more and more local consumption there. This will therefore push us to reevaluate our network of cities. It is of course too early to give details at this stage but this will clearly lead to a reworking of distribution.”

The new context in China should lead other luxury businesses to rethink their game plan for this strategic market. As Jourdan suggests, any brand which wants to conduct business in China will be interested in, “considering direct distribution in the country with an offer endowed with identical prices to those found in Europe or elsewhere while considering eventually conducting a part of its production in the country.”

Copyright © 2024 FashionNetwork.com All rights reserved.